A new set of research briefs has been released by the ARC Centre of Excellence in Population Ageing Research (CEPAR), examining the current state and projected future of Australia’s retirement incomes system.

The set of three new research briefs presents the latest data on retirement income in Australia and highlights new and relevant research in this area, featuring findings from over 40 of CEPAR’s leading researchers. The briefs focus on the public and private elements of retirement incomes provision. They take stock of the Age Pension and its poverty outcomes, discuss how Australians will be able to convert superannuation into retirement income, and assess existing financial behaviour of consumers and how best to guide them.

The Australian system compares well internationally

“The Australian retirement system is among the most sustainable and provides a more progressive level of replacement rates than seen in other countries. The system continues to score highly. But weaknesses identified to date have included a lack of requirement or incentive to take benefits as income streams, and incomplete provision of information to members,” said CEPAR Director and UNSW economist Scientia Professor John Piggott.

Improved standards of living in retirement

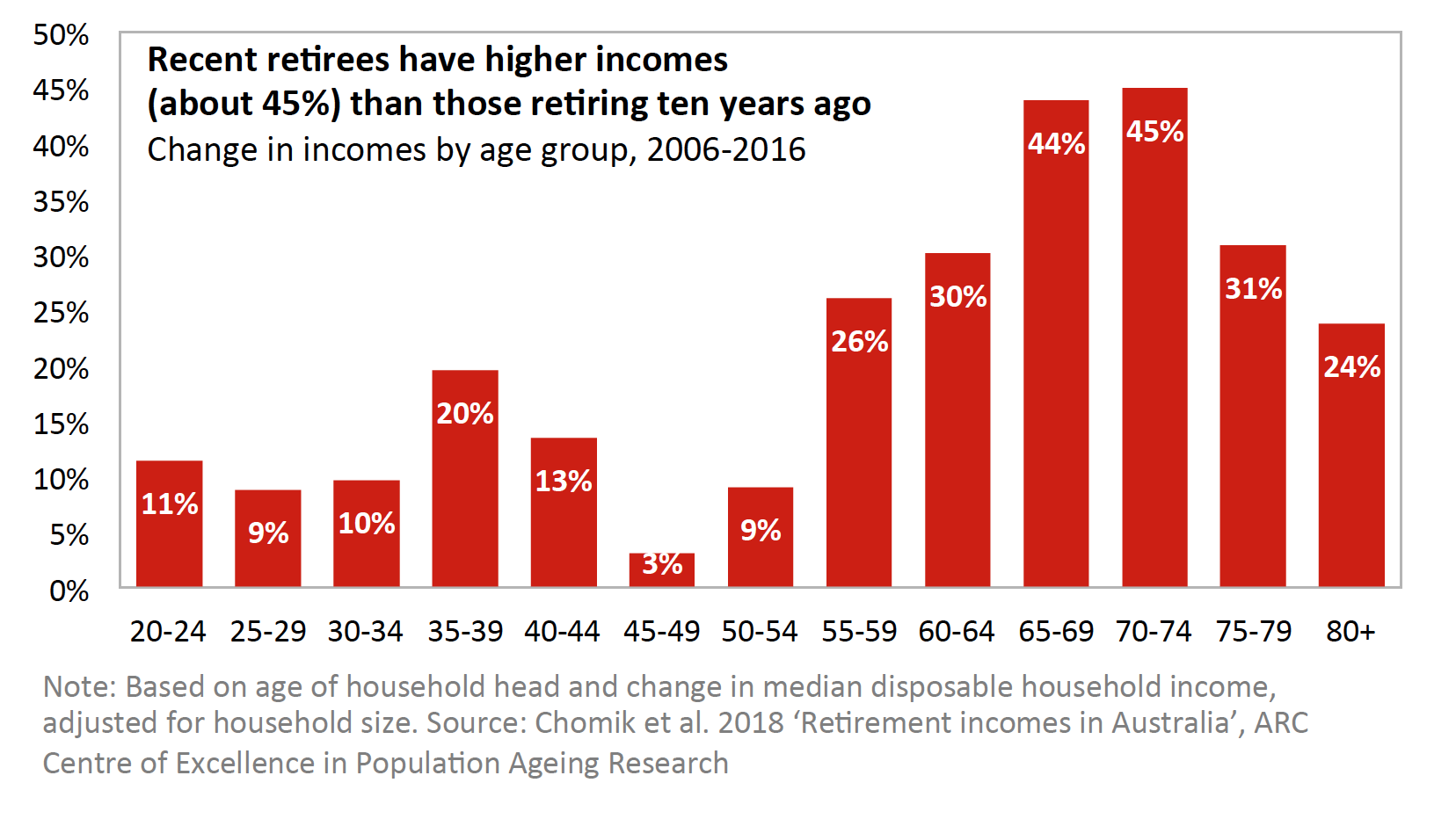

“Our analysis shows that standards of living of older people have improved over the last decade. About three in five older Australians can afford a lifestyle that is deemed to be above a modest level, according to a set of commonly used budget standards. And households reaching retirement age today have incomes about 45% higher than those reaching the same milestone ten years ago,” said Professor Piggott, a leading pension and retirement researcher and former member of the Henry Review panel.

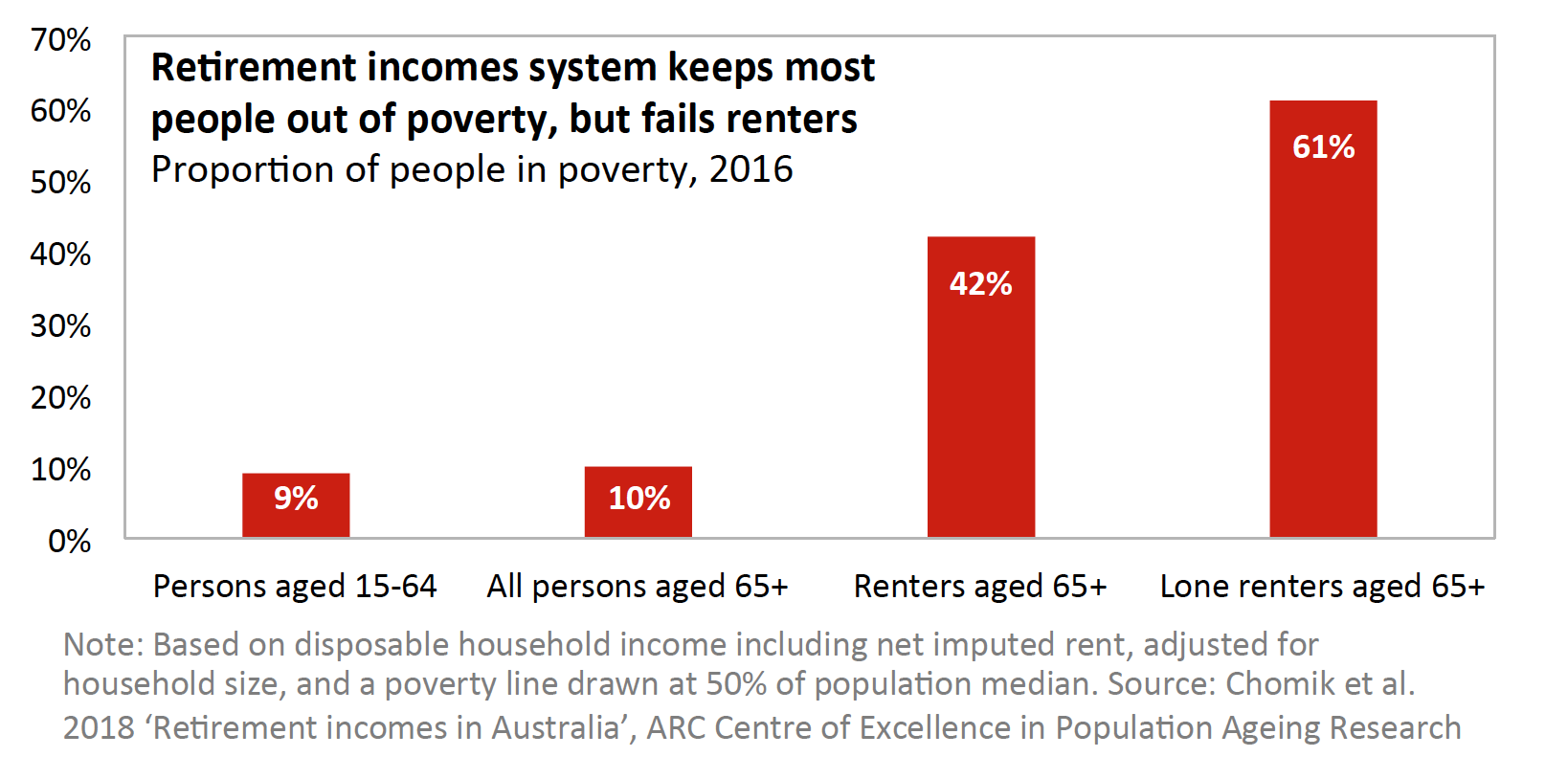

“The overall view is that the system is unique, broadly affordable and suitable for most Australians. It costs less than 3% of GDP and keeps most out of poverty, but not renters,” he said.

“Australian old age poverty is low once we take account of housing, but the system fails renters. Home owners are significantly better off than renters,” said lead author Rafal Chomik, CEPAR Senior Research Fellow at UNSW Sydney.

“About 60% of lone renters are in poverty, which translates to low standards of living. For example, a quarter of pensioners who rent alone spend on average less than $6 on food per day. Our analysis suggests an increase in rental assistance payments of 40% would reduce lone renter poverty by almost 20 percentage points, at a cost of about $380m,” Chomik said.

Superannuation is an integral part of retirement income but consumers find it complex and need guidance

“Australia is not ageing as fast as some countries, and boasts a retirement income system ranked among the best in the world. But it continues to be the subject of a series of reviews, reforms, and incremental refinements that seek to resolve remaining weaknesses,” said Professor Piggott.

“As population ageing moves from projection to reality and affects more people, any design flaws in retirement incomes systems will continue to attract attention by policymakers. CEPAR provides the research evidence base for policy reform to enable individuals, businesses and governments to respond better to demographic change and improve wellbeing,” he said.

The research briefs on retirement income in Australia are available to download at cepar.edu.au/resources-videos/research-briefs