A new set of research briefs has been released by the ARC Centre of Excellence in Population Ageing Research (CEPAR), examining the current state and projected future of Australia’s retirement incomes system. The third brief in the set, focused on private resources, highlights research on superannuation decumulation.

The set of three research briefs presents the latest data on retirement income in Australia and highlights new and relevant research in this area, featuring findings from over 40 of CEPAR’s leading researchers. The briefs focus on the public and private elements of retirement incomes provision, with research insights providing the evidence base for the design of superannuation decumulation products and models for policy reform.

“Much thought has gone into accumulating superannuation, less into its decumulation. Australia is the only OECD country that has a mandated pre-funded accumulation structure without a mandated decumulation structure,” said lead author CEPAR Senior Research Fellow Rafal Chomik.

“Yet how Australians spend their super is set to change in the next few years. A policy framework is under development to require fund trustees to offer risk-pooling products to members. For the superannuation sector, this could be a new opportunity. For government, it comes with concerns that the inefficiencies that have plagued the accumulation phase could also translate to inefficiencies in the retirement product market,” he said.

How to improve super decumulation

CEPAR Chief Investigator Michael Sherris, Professor of Actuarial Studies at UNSW Sydney, and his research group develop models for retirement risks aimed to support the design of sustainable cost-effective products that allow individuals to manage longevity, health and aged care risk.

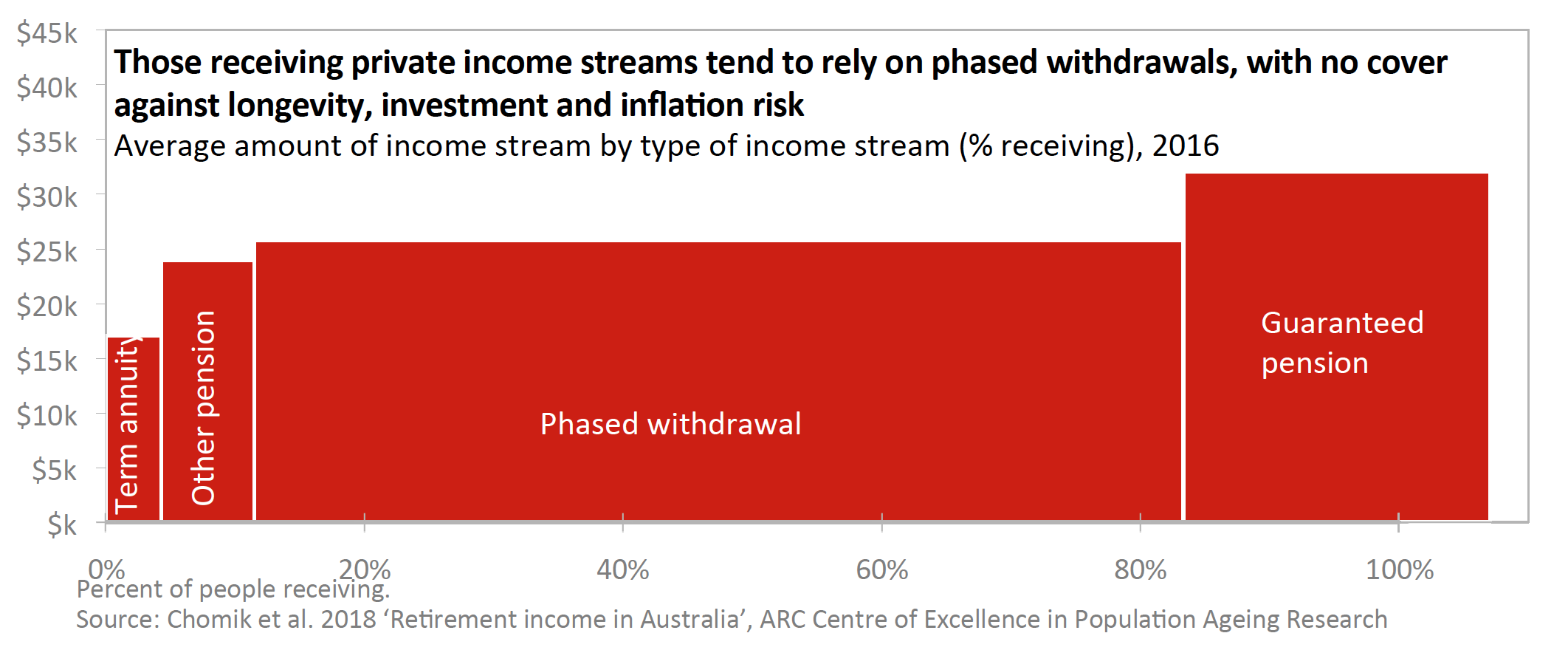

He said individuals don’t generally turn superannuation assets into retirement income products, leaving retirement risks with consumers, who by holding on to superannuation assets self-insure many retirement risks or rely on the government safety net. Those receiving private income streams tend to rely on phased withdrawals, with no cover against longevity, investment and inflation risk.

Product design innovations

Rafal Chomik said trustees would need to determine which retirement income products they offer their members. New retirement income products, such as pooled, deferred, long-term care, or variable annuities, aim to provide the combination of security and flexibility that individuals seek in retirement.

Professor Michael Sherris said while the availability of annuity products has grown, the demand for them has been lacklustre, and innovation in products is required to meet individual needs. Locking in current low interest rates in a fixed or life annuity is not necessarily the best way to generate retirement income.

“Individuals want flexibility, security and investment returns – something that a variable annuity product can deliver, although the guarantees in these products can be expensive. The US experience with these products suggests that such guarantees were too generous in the past and providers suffered unexpected losses. Appropriate design is therefore paramount, including investment strategies that target volatility,” he said.

“Ways to make annuities more attractive to members include pooling the longevity risk through pooled annuities, and pricing to recognise that the health and wealth of individuals impacts the cost, to the extent that regulations allow. This would mean more attractive pricing,” he said.

Research outlined in the research briefs also suggests that people are more willing to pay for an annuity after being provided with timely, balanced information, and the opportunity to learn about the key features.

“The preferred option is to prescribe a standard product that combines the flexibility of an account-based pension with the insurance of a deferred annuity. Other decumulation product options include group self-annuitisation or pooled annuities, and more effective guarantees that allow the consumer to take advantage of both strong investment returns and long-term security,” said CEPAR Chief Investigator Professor Sherris.

How should insurers forecast longevity risk and cope with mortality risk?

The research briefs also highlight a series of forecasting models developed by CEPAR researchers that consider causes of death, health and functional disability, multiple-populations, cohort based models and contain other technical innovations, relevant for life insurers, pension funds and regulators.

“These longevity risk models have made predicting cohort-level changes in mortality easier for insurers. Insurers need to both accurately forecast mortality rates and quantify the future variability of these rates, whether it is improving existing methods or proposing new techniques. Only then can innovative products that target longevity risk be adequately priced and brought to market,” said Sherris.

“For insurers, part of longevity cannot be easily diversified away by increasing portfolio size. As a result, insurers face systematic cash flow volatility, which may require higher capital and reserves, and lead to reducing profitability or insolvency.”

“We have considered several strategies for managing mortality risk for individuals, insurers and superannuation funds, that have been the subject of our research: reinsurance; securitization through insurance-linked securities; and holding reserve capital above the regulated level. We also looked at how government might help insurers cope with systemic risk by providing tail-end insurance or longevity bonds,” he said.

Decumulation policy is evolving

“Super decumulation is a live debate. Policies decided in the next few years will determine the future of superannuation decumulation in Australia, which is leading the world in policy that attempts to combine flexibility and government safety-net provision,” said Professor Michael Sherris.

“A range of retirement income products can provide a stream of resources in retirement, some of which are unavailable in Australia or operate in an inefficient market. These include products related to longevity risk insurance, long-term care insurance, and equity release products – all of which have been the subject of extensive research here at CEPAR and highlighted in our latest research briefs,” said Rafal Chomik.

The research briefs on retirement income in Australia are available to download at cepar.edu.au/resources-videos/research-briefs.